Dealing with roof damage can be a stressful task for any homeowner, especially in Florida, where storms and hurricanes are common. Understanding common roof insurance claims in Florida can help homeowners avoid delays, denials, and low settlement payouts. In this blog, Alpha Public Insurance Adjusters explains the mistakes homeowners often make after roof damage and how to better protect their claims.

Why Roof Insurance Claims Get Delayed

Roof insurance claims in Florida often face delays due to various factors. Understanding these can help you manage the process more efficiently. The main reason is the high volume of claims filed after a major storm or hurricane. Insurance companies become overwhelmed, leading to slower processing times.

Delayed Inspections

After a storm, it’s important to have your roof inspected promptly. Many homeowners delay inspections, either due to the assumption that the damage is minor or because they are unaware of the potential risks. Delayed inspections can lead to further damage, complicating your claim.

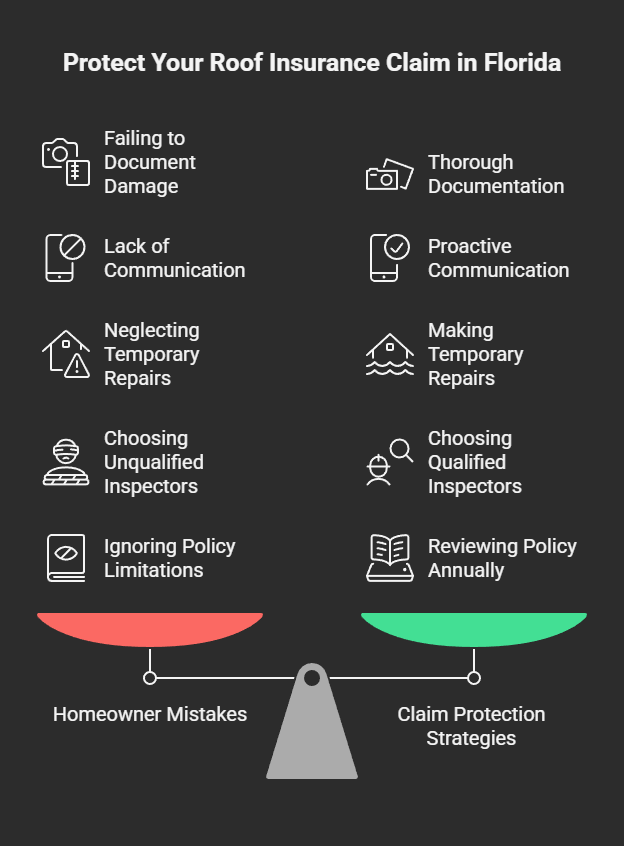

Lack of Communication

Another reason for delays is poor communication with your insurance company. It’s important to maintain regular contact, providing updates and responding quickly to requests for information. This proactive approach can help speed up the process.

Mistakes Homeowners Make After Storm Damage

Florida homeowners often make critical mistakes after their roofs sustain storm damage. Being aware of these can help you avoid them and ensure a smoother claims process.

Ignoring Minor Damage

Many homeowners ignore what appears to be minor damage, thinking it won’t affect their roof’s condition. However, even small issues can worsen, leading to bigger problems and higher repair costs. Always address any damage quickly to avoid complications.

Failing to Document Damage

Documentation is key when filing a roof insurance claim in Florida. Failing to document the damage adequately is a common mistake. Take clear, detailed photos and videos of all affected areas, and keep any relevant receipts or repair estimates.

Documentation Problems That Hurt Claims

Proper documentation is important for a strong roof damage insurance claim. Unfortunately, many homeowners miss key steps in this area, leading to denied roof claims or reduced settlements.

Insufficient Evidence

Providing insufficient evidence of the damage can weaken your claim. Ensure you capture every angle and detail of the damage. If possible, obtain before-and-after photos to clearly show the impact of the storm.

Inaccurate Information

Submitting inaccurate or incomplete information is another common mistake. Double-check all the details in your claim, including dates, descriptions, and personal information, to avoid avoidable problems.

Temporary Repairs & Inspection Issues

When dealing with roof damage, temporary repairs and inspections play an important role in the insurance claim process. However, handling these incorrectly can lead to problems.

Neglecting Temporary Repairs

It’s important to make temporary repairs to prevent further damage to your roof. Failing to do so can be seen as neglect, potentially affecting your claim. Use tarps or other materials to cover exposed areas and reduce additional damage.

Choosing Unqualified Inspectors

Hiring unqualified inspectors can result in inaccurate assessments, affecting your claim’s validity. Always choose certified professionals with a good reputation to ensure a proper inspection.

Why Insurance Companies Underpay Roof Claims

Insurance companies sometimes underpay roof claims, leaving homeowners with not enough funds to cover repairs. Understanding why this happens can help you take preventive measures.

Policy Limitations

Many policies have limitations or exclusions that homeowners are unaware of until it’s too late. Review your policy carefully to understand what is covered and what isn’t.

Discrepancies in Damage Assessment

Insurance adjusters may assess the damage differently than your contractor, leading to lower payout offers. Having a public adjuster from a company like Alpha Public Insurance Adjusters can help pursue a fair settlement.

How to Protect Your Insurance Claim

Taking early action can improve the outcome of your roof insurance claim in Florida. Here are some steps to protect your claim effectively.

Thorough Documentation

As highlighted earlier, thorough documentation is important. Maintain organized records of all communications, photos, and estimates related to your claim.

Engage a Public Adjuster

Consider hiring a public adjuster to represent your interests. These professionals have the experience and experience to handle negotiations and ensure you receive a fair settlement.

Review Your Policy Annually

Regularly reviewing your insurance policy helps you stay informed about your coverage and any changes. This knowledge can be very useful when filing a claim.

For more information on roof damage claims, hurricane damage claims, or to consult with a public adjuster, visit our pages on Roof Damage Claims, Hurricane Damage Claims, and Public Adjusters.

Understanding and avoiding these common mistakes can save Florida homeowners time, money, and stress when dealing with roof damage insurance claims. By being proactive and informed, you can navigate the claims process more effectively and secure the compensation you deserve.

For expert assistance, contact Alpha Public Insurance Adjusters today, where we are dedicated to helping you manage your insurance claims efficiently.

Stay informed, stay prepared, and protect your home with the right knowledge and resources.

FAQs

- What should I do immediately after storm damage? Conduct a thorough inspection, document the damage, and initiate temporary repairs to prevent further issues.

- How can I ensure my claim isn’t underpaid? Engage a public adjuster to advocate on your behalf and ensure a fair assessment of your damages.

- Why are roof claims often denied? Claims can be denied due to insufficient documentation, policy exclusions, or missed deadlines.